Master Class on a VA IRRRL – Streamline Refinance

Understanding the IRRRL: Three Main Criteria

- Interest Rate Reduction: Your new interest rate must be at least half a percentage point lower than your current rate. For instance, if you’re at 6%, your new rate should be 5.5%.

- Seasoning Requirement: You must have made at least six consecutive monthly payments and 210 days must have passed since your first payment.

- Cost Recoupment: You should be able to recover all closing costs within 36 months from the savings achieved by refinancing.

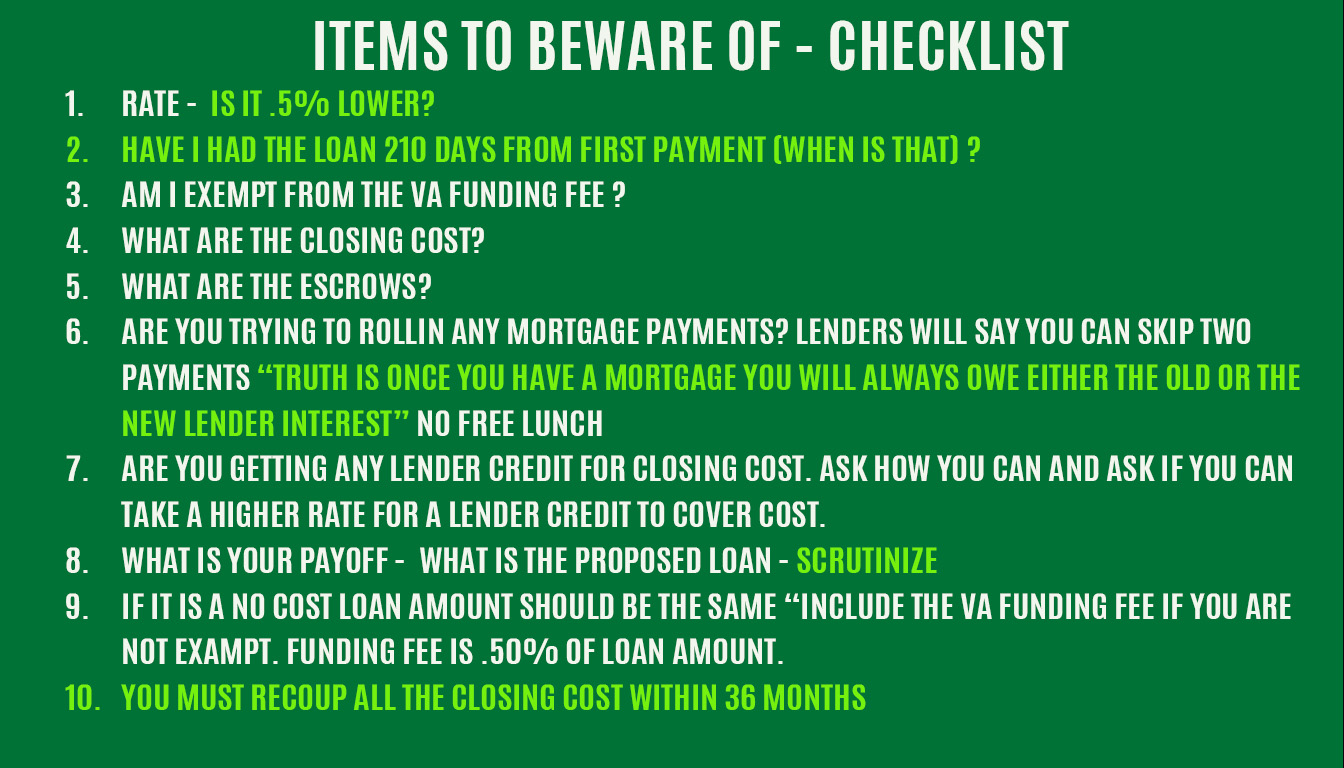

10 Essential Checklist Items for Your VA IRRRL

- Interest Rate Check: Ensure your new rate is at least 0.5% lower.

- Loan Duration: You must have held your loan for at least 210 days from your first payment.

- VA Funding Fee Exemption: Verify if you are exempt and if you have paid a funding fee previously.

- Transactional Closing Costs: Understand your non-recoverable closing costs such as credit reports and recordation charges.

- Escrow Obligations: Know your escrow requirements to avoid cash out unexpectedly.

- Skipping Payments: Be cautious; you never truly skip a payment—it’s rolled into your loan.

- Lender Credit: Aim for a credit covering your closing costs and VA funding fee.

- Payoff Understanding: Know your exact payoff to avoid surprises at closing.

- No Cost vs. No Cash: Clarify if ‘no cost’ loans truly cover additional costs or roll them into your loan.

- Protection Rule: Ensure you recoup costs within 36 months to maintain loan effectiveness.

Additional Insights

VA loans are versatile and beneficial, even if your property becomes an investment. If your property was a primary residence, you can still access IRRRL benefits post-relocation.

About the Author

Kevin Retcher, a veteran-owned mortgage broker in Virginia, specializes in VA loans across Virginia, Maryland, and DC. With a network spanning 32 states, Kevin’s insights are invaluable for navigating VA loan intricacies.

For personalized guidance and checking live rates, reach out or visit Kevin’s website. His commitment to helping fellow veterans is rooted deeply in understanding their unique financial needs.

Conclusion

The VA IRRRL is an exceptional tool for financial savings and stability for veterans. Use these guidelines to navigate your refinancing options effectively. Embrace the strategy Gen Z veterans are already leveraging, ensuring your financial journey is both strategic and rewarding. Remember, as Kevin says: “Semper Fi.”